Does higher risk lead to better long-term returns?

Many investors operate under a common assumption: to achieve higher returns over the long run, one must take more risk and invest aggressively, usually by piling into hot growth stocks. On the surface, this logic holds up. Aggressive portfolios often soar during bull markets, while conservative portfolios can feel slow, uninspired, and unimpressive by comparison. However, this perspective ignores one of the most powerful forces in finance: compounding.

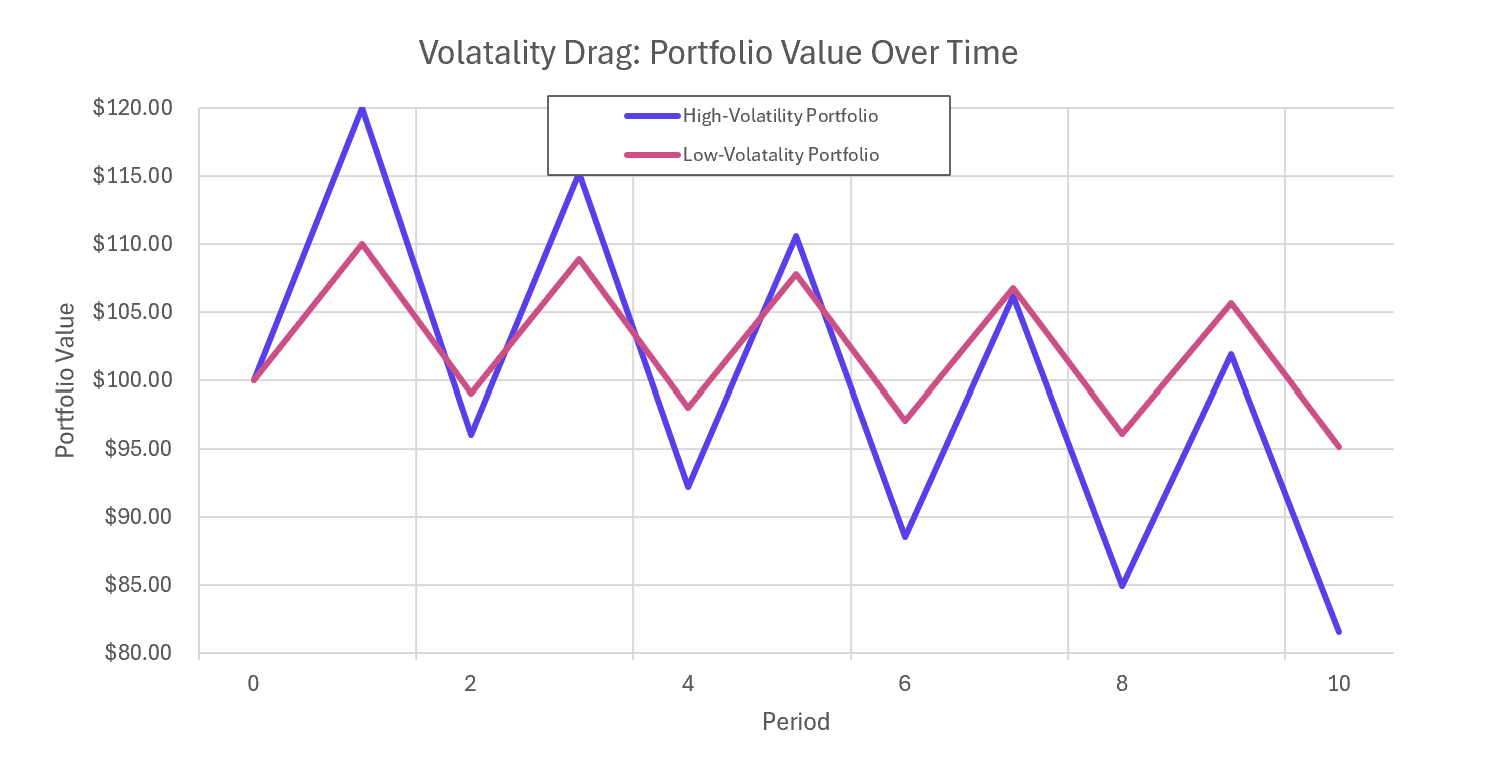

A Tale of Two Strategies: Alex vs. Ben

To explore how differences in portfolio volatility can affect long-term compounding under certain assumptions, let’s look at a simplified illustration involving two hypothetical investors.

The example is hypothetical and provided solely for illustrative purposes. It does not represent actual investment performance, is not based on any specific portfolio, and does not reflect the impact of advisory fees, transaction costs, taxes, or changing market conditions. Actual investor outcomes will vary and may differ materially from the results shown.

Alex: The Aggressive Investor

Alex seeks growth and excitement. His portfolio is heavily tilted toward growth stocks and is prone to dramatic price swings. He enjoys the high of a surging market but is exposed to significant downside risk.

Ben: The Steady Investor

Ben prioritizes stability. His portfolio is well diversified but exhibits lower volatility because it contains a healthy proportion of value stocks. While he never tops the performance charts during good years, he avoids the severe capital destruction that occurs during bad years.

The twist: On paper, both portfolios earn the exact same average return over time. But who ends up with more wealth?

The Mathematical Reality of Volatility Drag

Volatility is more than just a measure of risk; it is a measure of how much a portfolio fluctuates. This matters because investment returns compound; they are not simply additive. To see this in action, let’s compare how Alex & Ben’s portfolios behave starting with an initial investment of $100,000.

| Year | Alex (High Volatility) | Ben (Low Volatility) |

|---|---|---|

| Year 1 | +20% ($120,000) | +10% ($110,000) |

| Year 2 | -20% ($96,000) | -10% ($99,000) |

| Average Return | 0% | 0% |

| Actual Value | $96,000 | $99,000 |

Even though their average returns were the same (0%), Alex lost $4,000 of his principal, while Ben only lost $1,000.

If similar return patterns were to persist over time, differences in volatility could lead to divergent results, highlighting how drawdowns may affect long-term compounding under certain conditions. Alex’s portfolio slowly grinds lower due to a phenomenon known as volatility drag. Ben’s portfolio finishes higher not because it was smarter, but because it was steadier.

Of course, when investing, other factors such as goals, risk tolerance, time horizon, and the full portfolio context play a strong role in making portfolio investment decisions. The above illustration is to explain the counterintuitive concept and its impact which most people miss.

Why Losses Hurt More Than Gains Help

The math of investment growth is skewed against the aggressive investor. Because of how percentages work, a large loss requires a much larger subsequent gain just to break even:

- To recover from a 10% loss, you need an 11% gain.

- To recover from a 25% loss, you need a 33% gain.

- To recover from a 50% loss, you need a 100% gain.

Alex’s large swings cause deeper drawdowns, which may curtail the power of compounding. Ben’s portfolio doesn’t need to stage a miraculous recovery because it never dug a deep hole to begin with. Larger portfolio swings can result in deeper drawdowns, which may make recovery more challenging and impact long-term compounding, depending on market conditions and investor behavior.

The Human Element: Behavior Compounds Too

Beyond mathematics, low volatility offers a psychological advantage. Real-world investing involves human emotion, and when markets crater, behavior often becomes the biggest risk factor.

- The Aggressive Investor: During a crash, Alex feels immense stress. Sticking to the plan becomes difficult, and the prospect of rebalancing into a falling market feels painful.

- The Steady Investor: Ben notices the decline, but the impact is manageable. He can rebalance his portfolio with a clear head and stay invested for the long term.

Conclusion: The Real Question for Investors

Does taking more risk lead to better returns? Sometimes. But it comes out ahead less often than people assume.

Aggressive portfolios may look superior in a bull market, but they suffer more in downturns, experience higher volatility drag, and require massive recoveries just to stay even. Steadier portfolios may rise less in good years but fall significantly less in bad ones. By avoiding deep losses, they recover faster and tend to compound more efficiently across full market cycles.

When evaluating your strategy, don’t ask: “Which portfolio wins in the best years?” Instead, ask: “Which portfolio has the potential to compound most efficiently across all types of investment environments?”

Time and again, the answer tends to be: Steady wins. Not by being flashy, but by being durable.