“Can’t I just put my money in an index fund and call it a day?”

If you’ve ever wondered whether paying a financial planner is worth it, you’re not alone. After all, why pay someone year after year when you could invest in a simple index fund yourself or pay for one-time advice and be done with it?

Here’s the truth that might surprise you: If you think a financial planner’s job is just picking stocks and funds, you’re missing about 80% of what they do.

Most people assume financial planners are glorified stock pickers. But investment management? That’s actually a small part of the equation.

In my previous post on Investment Management vs. Wealth Management, I broke down the critical difference between these roles. Wealth managers (also called financial planners) focus on the big picture—your complete financial life, not just your portfolio.

Think of it this way: You wouldn’t hire a personal trainer just to tell you which gym equipment to use. You hire them for the customized workout plan, the accountability, the form corrections, and the motivation when you want to quit.

A financial planner works the same way—but for your money.

What You’re Truly Paying For

Just like a primary care physician knows your medical history, family background, and health goals, your financial planner becomes the person who truly understands your life. They know:

- What keeps you up at night

- What you’re working toward

- What trade-offs you’re willing (and unwilling) to make

- How your situation changes as life throws curveballs

And they bring professional expertise to help you succeed as laws change, markets fluctuate, and your personal circumstances evolve.

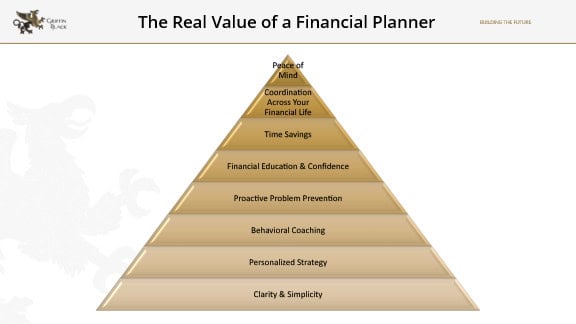

Here’s the value breakdown that actually matters:

1. Clarity & Simplicity

Your financial life may feel like a tangled mess of accounts, goals, tax considerations, and endless decisions. A good planner cuts through the noise and shows you a clear path forward.

Instead of lying awake wondering “Am I saving enough for retirement?” while juggling multiple spreadsheets, your planner tells you how much you are likely to need, when to adjust your contributions, and what trade-offs you’re actually facing. No more guesswork. Just clarity.

2. Personalized Strategy (Because You’re Not a Template!)

Every cookie-cutter financial plan available on the web is essentially useless. Why? Because no two lives are identical. Your goals, values, family dynamics, career trajectory, risk tolerance, and timeline are uniquely yours.

Maybe you dream of retiring at 50 to travel the world. Your neighbor wants to fund their child’s medical school and start a side business. Your colleague is focused on caring for aging parents while building wealth. Oh, and only one of them thinks it’s important to have something to leave to their kids.

Same income, totally different plans. Your financial planner builds a strategy that fits your life – not a generic template pulled from a TikTok ‘expert’.

3. Behavioral Coaching (AKA Saving you from yourself)

The biggest threat to your financial success isn’t market crashes. It’s your own emotions.

Markets swing wildly. Fear and greed whisper in your ear. FOMO kicks in when everyone else seems to be getting rich on the latest trend. A planner keeps you grounded and prevents impulsive decisions that could derail decades of progress.

For example, when the market drops 20% and panic sets in, your instinct might scream “SELL EVERYTHING!” Your planner calmly reminds you of your long-term strategy, shows you historical data, and helps you stay the course or even take advantage of the dip.

Vanguard Study1 shows that informed behavioral coaching alone can add 1-2% to annual returns. Over 30 years, that’s significant.

4. Proactive Problem Prevention

Financial mistakes are expensive. Sometimes catastrophically so.

Your planner helps you avoid costly pitfalls like:

- Missing critical tax deadlines

- Underinsuring your most valuable assets

- Forgetting to update beneficiaries after major life events

- Making premature retirement account withdrawals

- Overlooking estate planning updates

Your planner notices your estate plan hasn’t been updated since your second child was born three years ago. That one catch-up saves your family from potential legal nightmares and ensures your assets go where you actually want them to go.

Prevention is invisible—until something goes wrong.

5. Financial Education & Confidence

You don’t need to become a financial expert. That’s literally what you’re paying someone else to be. But you do need to understand your options and feel confident in your decisions.

Your planner translates complex financial jargon into plain English and helps you make informed choices.

Should you do a Roth conversion this year? When should you start taking Social Security? Is refinancing your mortgage worth it?

Oh, and by the way, if you’re thinking about buying an index fund, which index fund is likely to be the best one for you? Do you know why you should be buying a particular index, which funds maintain low tracking error and are priced well? Etc., etc.

Your planner breaks down the pros, cons, and math – without making you feel like you need a PhD to understand it.

6. Time Savings

Researching financial strategies is time-consuming and, for most people, mind-numbingly boring. Your planner does the heavy lifting:

- Analyzing options across accounts and strategies

- Coordinating with your CPA, attorney, and insurance agent

- Staying current on tax law changes and new regulations

- Monitoring your progress and adjusting as needed

Instead of spending your weekends falling down Google rabbit holes about the latest tax law changes, your planner updates your strategy and sends you a simple action list.

7. Coordination Across Your Financial Life

Your money doesn’t exist in silos. Everything connects.

Your financial planner acts as the quarterback, making sure your:

- Tax strategy

- Investment approach

- Insurance coverage

- Estate plan

- Retirement timeline

- Education funding

…all work together harmoniously instead of working against each other.

When you sell a rental property, your planner coordinates with your CPA to minimize the tax hit and reinvest the proceeds strategically – rather than letting that cash sit in your checking account or making a hasty investment decision.

8. Peace of Mind

The biggest value might be purely emotional.

Knowing someone is actively watching out for your financial well-being lets you sleep better at night. You’re not crossing your fingers and hoping you’ll be okay in retirement.

You are confident you will be—because you have a plan and a professional guiding you through it.

And here’s why this matters more than you might think: Time compounds everything. Small errors that seem insignificant today can cost you hundreds of thousands of dollars over decades. Having a professional in your corner magnifies good decisions and prevents costly mistakes from snowballing.

So, Does Everyone Need a Financial Planner?

The honest answer: Yes and no.

You might benefit if you:

- Feel overwhelmed by your financial situation

- Want clarity on whether you’re on track

- Are facing major life transitions (career change, inheritance, divorce, retirement)

- Have multiple financial goals competing for limited resources

- Want to optimize your tax situation

- Need accountability and behavioral coaching

- Value your time and would rather delegate financial management

You might not need one (yet) if:

- Your financial life is genuinely simple (one job, one account, minimal assets)

- You genuinely enjoy diving deep into financial research

- You have the discipline to stick to a plan without outside accountability

That said, even if you don’t need a planner right now, it’s valuable to know professional advice exists. When your financial life becomes complex enough to warrant help, you’ll know exactly where to turn.

Understanding the Fee Structure

Most financial planners use a pricing model that’s straightforward: Assets Under Management (AUM). Here’s what many people get wrong: They see that percentage and think, “I’m paying X% for investment returns.”

Wrong!

You’re paying for:

- Comprehensive financial planning

- Strategic coordination across your entire financial life

- Behavioral coaching during market turbulence

- Proactive problem prevention

- Time savings and peace of mind

- Professional expertise adapting to your changing circumstances

Investment management is just one ingredient in the full recipe. And the effective cost to you actually decreases as your wealth grows.

Studies by Vanguard2, Morningstar3, and SmartAsset4 show that working with a financial planner can add 1.5%–3% in annual returns through strategies like tax efficiency, behavioral coaching, and optimized withdrawals far outweighing typical advisory fees. Research also highlights long-term benefits such as higher lifetime wealth (up to 113% more), greater financial security, and reduced stress, making professional advice a clear value proposition.

Think of the fee as insurance against costly mistakes, payment for clarity in complexity, and an investment in your own peace of mind. The real return you’re getting? It’s measured in confidence, time saved, stress avoided, and a financial life that actually works toward your definition of success.

And that’s a return you can’t put a price on.

Sources & Further Reading:

- Vanguard, “Putting a value on your value: Quantifying Vanguard Advisor’s Alpha®” (July 2022) ↩︎

- Vanguard, “The Value of Personalized Advice” (August 2022) ↩︎

- SmartAsset, “The Value of a Financial Advisor: What’s It Really Worth?” (January 2025) ↩︎

- Morningstar, “Alpha, Beta, and Now… Gamma” by David Blanchett and Paul Kaplan, The Journal of Retirement (2013) ↩︎

Disclaimer: This post is for educational purposes only and does not represent personalized financial advice. Past experiences, do not guarantee future outcomes. For advice tailored to your situation, please contact a qualified advisor.