The American Rescue Plan was signed into law on March 11 and there are several provisions that create tax planning opportunities. Here is a review of the most significant provisions for individuals.

Recovery Rebates

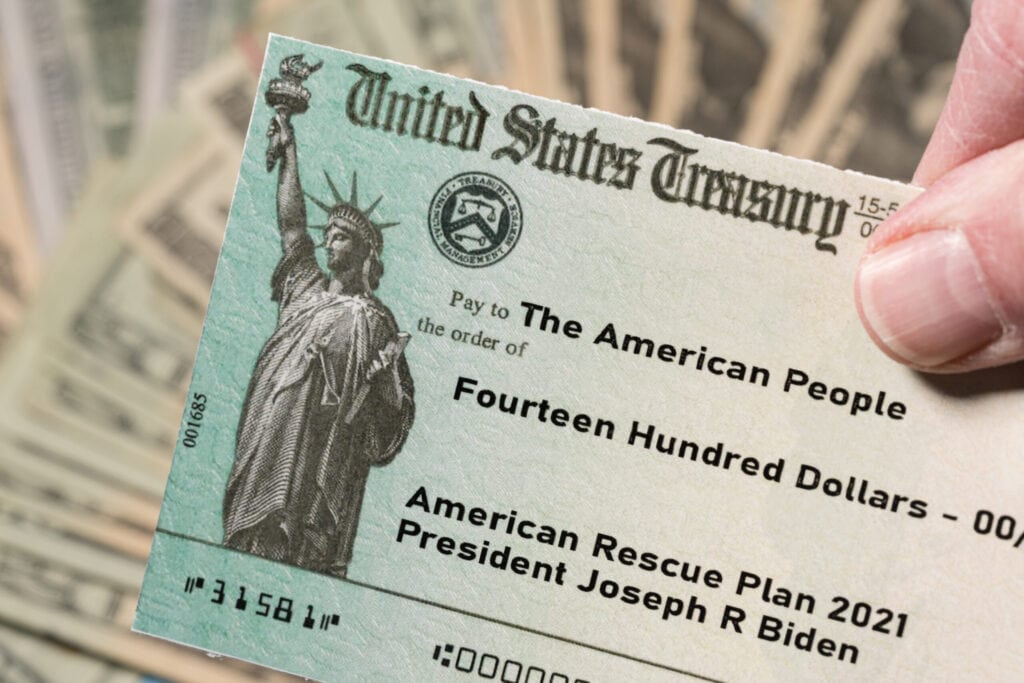

The new stimulus bill includes a rebate payment of $1,400 per person including dependents. Your income must fall below these thresholds to qualify for a rebate payment:

- $75,000 – $80,000 for single filers and married filing separately

- $112,500 – $120,000 for head of household

- $150,000 – $160,000 for married filing jointly

Determining if you qualify is a three-step process. Here’s how to take the most advantage of what’s offered:

- If your 2019 income is below the threshold and your 2020 income is not, delay filing your 2020 tax return until after you receive the rebate payment. Payments are being distributed as of this week.

- If your 2019 income is above the threshold and your 2020 income is below it, file your 2020 tax return as soon as you can. If you do not file your 2020 tax return by July 15, you will not be able to qualify for the rebate payment using your 2020 income.

- If your 2019 income and your 2020 income is above the threshold, but your 2021 income is below it, you will receive the rebate payment as a tax credit on your 2021 tax return.

Since your 2021 income can be used to qualify for the rebate payment, this creates tax planning opportunities:

- If your 2021 income will be slightly above the threshold, look for ways to reduce your 2021 income. Possible methods include increasing your contributions to retirement accounts, taking additional business deductions if you’re self-employed, asking your employer to delay your bonus payments until 2022, or taking a short unpaid sabbatical from work.

- If you took a COVID related distribution from your IRA or 401(k) in 2020 and elected to be taxed over a 3 year period, pay part of the distribution back in 2021 so that it does not count against your 2021 income. This might help you qualify for the rebate payment.

- If you have an older dependent with low income, let them support themselves in 2021 to qualify for their own rebate payment. This could include children in college or adult children living at home. If they pay for more than half of their own support, they are no longer your dependent. Contact your advisor for advice on how to transition your dependent into being independent for income tax purposes.

Child Tax Credit

The Child Tax Credit has been increased for 2021 to $3,600 per child under age 6 and $3,000 per child between ages 6-17. The credit starts to phase out if your income exceeds these thresholds:

- $75,000 for single filers and married filing separately

- $112,500 for head of household

- $150,000 for married filing jointly

If your 2020 income is below the threshold, you may receive an advance partial payment of the credit in July. However, you may have to pay back the advance if your 2021 income is over the threshold. If your 2021 income is slightly above these thresholds, look for opportunities to reduce your income before the end of the year.

Child and Dependent Care Tax Credit

The credit for childcare expenses has also been increased for 2021 and could be worth as much as $8,000. Also, the credit does not start to phase out until your income exceeds $125,000. This threshold is the same for all filing statuses. This creates a situation where it might be advantageous for married couples to change their filing status to married filing separately. Your CPA should run both scenarios to see which filing status is best. Again, look for opportunities to keep your 2021 income below the threshold if you are close to qualifying for this credit.

Unemployment Benefits

Federal unemployment benefits have been extended to September 6, 2021. If your state benefits are scheduled to expire, the new stimulus plan will extend them to September. You will also continue to receive the extra $300 per week benefit until September. This extension also applies to self-employed individuals.

If you received unemployment benefits in 2020, $10,200 from those benefits can be excluded from your taxable income. However, this only applies if your 2020 income is less than $150,000. This threshold applies to all filing statuses, so this is another case where filing separately instead of jointly may be beneficial. If you have already filed your 2020 tax return, you may amend it and get a tax refund. If you have questions about any of these provisions, how they apply to your situation, and how you can take best advantage of them, please contact your Griffin Black advisor.

Picture by Steve Heap on shutterstock.com